EM OPPORTUNITIES OR ESG CHALLENGES?

Most investors need little persuading that emerging markets offer exciting opportunities. But emerging markets also pose challenges so significant and entangled that investors are reminded of the legendary Gordian knot. Some challenges—such as inconsistent regulations and a lack of standardization across countries—reflect the diverse nature of emerging markets. Others, such as the seemingly intractable problems of pollution and corruption, are ESG risks.

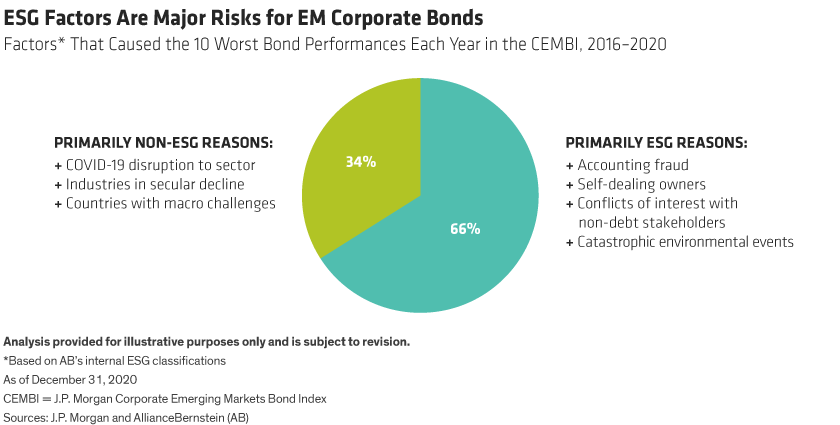

This is particularly relevant for investors in EM corporate bonds. Our analysis shows that more than half of the worst-performing credits in the J.P. Morgan Corporate Emerging Markets Bond Index (CEMBI) during the last five years were those with weak ESG practices (Display).

Given these challenges, why would anyone want to invest in EM corporate bonds? There are five reasons, in our view. Some of the most compelling are ESG-related.

First, the ESG risks to investing in EM corporates should be kept in perspective. Not all EM companies are ESG laggards. Mexican chemical company Orbia Advance, for example, has some of the lowest emissions and most ambitious carbon-reduction plans in its industry—indeed, better than those of many leading US and European chemical companies.

Second, there is a strong case for thematic investing in emerging economies. It may seem counterintuitive, given the perceived ESG risks of EM corporate bonds, but investing in emerging economies can help finance the world’s transition to greater social and environmental sustainability.

Emerging countries are home to about 70% of the world’s population and own a large share of the resources that will help drive the transition to a cleaner-energy future. For example, they produce 80% of the world’s copper—demand for which is expected to rise 50% during the next 20 years—and more than half of all lithium, for which demand is expected to double by 2024. Further, EM investing can support sustainable growth and social empowerment in some of the least developed parts of the world, by contributing to better health and educational opportunities.

Third, given a sufficiently robust research methodology and investment process, it’s possible to identify and manage the ESG and other risks associated with EM corporates. Such capabilities can identify opportunities as wells as risks, making EM corporate bonds a rational and attractive proposition—not only for investors who are explicitly targeting responsible-investment outcomes but also for those who are primarily concerned with capturing competitive risk-adjusted returns.

Fourth, EM corporate bonds compare favorably on many points with developed-market (DM) bonds. From 2015 to 2020, for example, the CEMBI had a Sharpe ratio—a measure of return per unit of risk—double that of EM sovereign bonds. Similarly, the Sharpe ratios for the high-yield and investment-grade portions of the CEMBI were higher than those of their DM equivalents. EM corporate bonds’ credit quality compares favorably, too. On average, investment-grade EM credit ratings have been catching up with the average rating of US investment-grade corporate bonds.

Fifth, EM bonds provide portfolio diversification. The EM corporate bond market comprises more than US$2.5 trillion of international US-dollar bonds across more than 600 companies. That’s considerably larger than the EM sovereign debt market and as big as the US-dollar and euro high-yield markets combined. EM corporate bonds also have low correlations to other corporate bond markets.

In our view, the key to identifying and managing the risks of the EM corporate bond market lies in applying a deep and rounded research methodology and investment process, with ESG factors fully integrated into both. We discuss below how investors can combine comprehensive credit analysis and ESG research to clarify the risks and potentially benefit from the opportunities presented by EM corporate bonds.

ESG RATINGS OFFER ONLY PARTIAL INSIGHTS

When developing an ESG-aware research and investment process for EM corporate bonds, the first point to consider is data—its availability, comprehensiveness, accuracy and comparability. Many EM companies are majority owned by families or governments, and so are subject to less demanding disclosure requirements than those that apply to publicly listed entities. This can be a challenge for investors who attempt to carry out their own research. It can also present challenges to EM indices.

Because of this, many investors turn to ESG rating agencies that—rather like traditional credit rating agencies—analyze companies’ ESG risks and assign ratings as a guide for investors. While such ratings can be helpful, they may be misleading or confusing if taken at face value, for two reasons. First, the agencies face the same problems as investors in trying to acquire the necessary data. And second, there can be significant differences in the way agencies assess the risks.